Blog

TOP POSTS

Health Insurance for Unemployed Individuals

American’s as a whole already have staggeringly high rates of individuals who lack health insurance. There are many reasons for […]

Recent

Auto Insurance

SR-22 Insurance in Maricopa: What Arizona Drivers Need to Know

What Is SR-22 Insurance—And Why Maricopa Drivers May Need...

June 19, 2026Auto Insurance, Business Insurance, Health Insurance, Home Insurance, Insurance, Life Insurance, Mobile Home Insurance

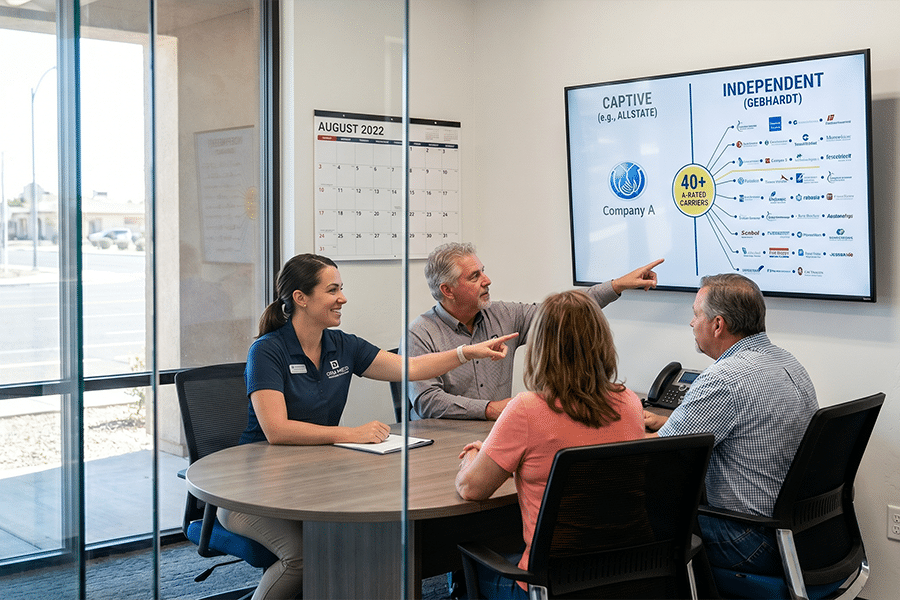

Allstate vs. Gebhardt Insurance: Which Is the Best Choice for Casa Grande and Maricopa Residents?

If you’re shopping for auto, home, or mobile home i...

May 15, 2026Health Insurance

Auto Insurance, Business Insurance, Health Insurance, Home Insurance, Insurance, Life Insurance, Mobile Home Insurance

Auto Insurance, Business Insurance, Health Insurance, Home Insurance, Insurance, Life Insurance, Mobile Home InsuranceAllstate vs. Gebhardt Insurance: Which Is the Best Choice for Casa Grande and Maricopa Residents?

May 15, 2026

Recent

Auto Insurance

SR-22 Insurance in Maricopa: What Arizona Drivers Need to Know

What Is SR-22 Insurance—And Why Maricopa Drivers May Need...

June 19, 2026Auto Insurance, Business Insurance, Health Insurance, Home Insurance, Insurance, Life Insurance, Mobile Home Insurance

Allstate vs. Gebhardt Insurance: Which Is the Best Choice for Casa Grande and Maricopa Residents?

If you’re shopping for auto, home, or mobile home i...

May 15, 2026