Blog

TOP POSTS

Factors that Affect Homeowners Insurance Premiums

Living in America, we are taught that we can do, be, and accomplish anything we put our minds to if […]

Recent

Auto Insurance

SR-22 Insurance in Maricopa: What Arizona Drivers Need to Know

What Is SR-22 Insurance—And Why Maricopa Drivers May Need...

June 19, 2026Auto Insurance, Business Insurance, Health Insurance, Home Insurance, Insurance, Life Insurance, Mobile Home Insurance

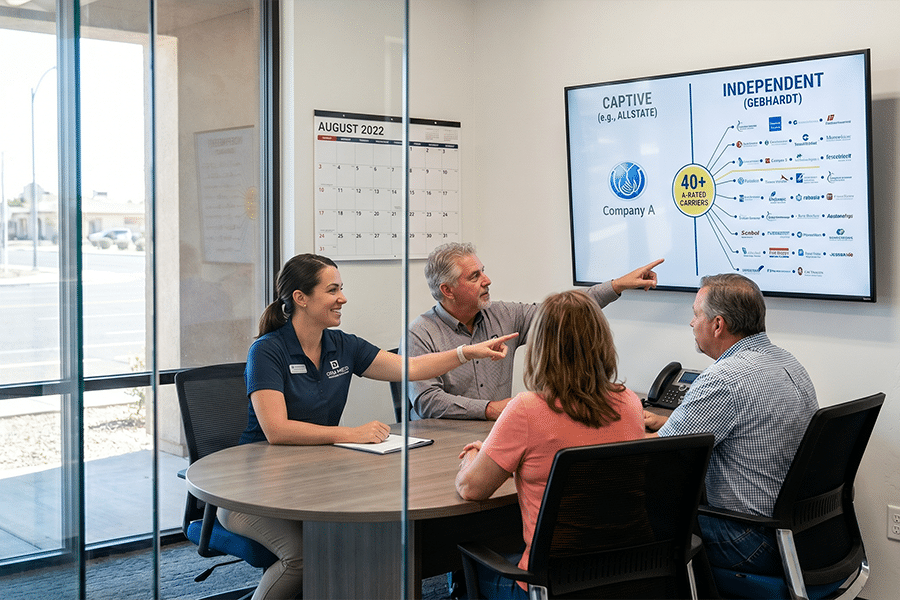

Allstate vs. Gebhardt Insurance: Which Is the Best Choice for Casa Grande and Maricopa Residents?

If you’re shopping for auto, home, or mobile home i...

May 15, 2026Home Insurance

Auto Insurance, Business Insurance, Health Insurance, Home Insurance, Insurance, Life Insurance, Mobile Home Insurance

Auto Insurance, Business Insurance, Health Insurance, Home Insurance, Insurance, Life Insurance, Mobile Home InsuranceAllstate vs. Gebhardt Insurance: Which Is the Best Choice for Casa Grande and Maricopa Residents?

May 15, 2026 Auto Insurance, Home Insurance

Auto Insurance, Home InsuranceWhy You Should Bundle Auto and Home Insurance: A Complete Guide for Casa Grande & Maricopa Homeowners

April 17, 2026 Insurance, Auto Insurance, Business Insurance, Home Insurance, Liability Insurance, Mobile Home Insurance

Insurance, Auto Insurance, Business Insurance, Home Insurance, Liability Insurance, Mobile Home InsuranceComplete Insurance Checklist for Snowbirds & Winter Visitors in Casa Grande & Maricopa, Arizona

December 19, 2025Recent

Auto Insurance

SR-22 Insurance in Maricopa: What Arizona Drivers Need to Know

What Is SR-22 Insurance—And Why Maricopa Drivers May Need...

June 19, 2026Auto Insurance, Business Insurance, Health Insurance, Home Insurance, Insurance, Life Insurance, Mobile Home Insurance

Allstate vs. Gebhardt Insurance: Which Is the Best Choice for Casa Grande and Maricopa Residents?

If you’re shopping for auto, home, or mobile home i...

May 15, 2026 Auto Insurance, Business Insurance, Home Insurance, Insurance, Renters Insurance

Auto Insurance, Business Insurance, Home Insurance, Insurance, Renters InsuranceSummer in Casa Grande & Maricopa: Why Insurance Matters More Than Ever

April 10, 2025 Home Insurance

Home InsuranceMaricopa Home Insurance Made Easy: How Gebhardt’s Local Experts Find Your Best Coverage

March 20, 2025Stay in touch with us

And get a free quote!

Auto Insurance, Business Insurance, Home Insurance, Mobile Home Insurance, Motorboat Insurance, Motorcycle Insurance, Renters Insurance

Auto Insurance, Business Insurance, Home Insurance, Mobile Home Insurance, Motorboat Insurance, Motorcycle Insurance, Renters InsuranceStruggling to Find Specialized Coverage? Insurance Agents in Maricopa, AZ Have You Covered

January 21, 2025 Business Insurance, Home Insurance, Life Insurance

Business Insurance, Home Insurance, Life InsuranceTop 5 Reasons Casa Grande Residents Need Customized Insurance Coverage

December 16, 2024 Auto Insurance, Home Insurance, Mobile Home Insurance

Auto Insurance, Home Insurance, Mobile Home InsuranceHow Casa Grande Insurance Brokers Simplify Coverage for Arizona Snowbirds

December 9, 2024 Auto Insurance, Business Insurance, Home Insurance

Auto Insurance, Business Insurance, Home Insurance